The Scaled Tariff: A Mechanism for Combating Mercantilism and Producing Balanced Trade

Jesse T. Richman

Department of Political Science

Old Dominion University

jrichman@odu.edu

Howard B. Richman

Ideal Taxes Association

howard@idealtaxes.com

Raymond L. Richman

Graduate School of Public and International Affairs

University of Pittsburgh

richmanpitt@aol.com

Abstract

In this paper we first discuss whether or not the modern form of mercantilism that contributes to the trade deficit of the United States and other countries is a self-destructive and thus self-correcting strategy. We argue that it is not self-correcting. Then we discuss mechanisms that a trade deficit country could utilize in order to produce balanced trade. The mechanisms differ in six respects, with the Scaled Tariff excelling in each.

Key words: Mercantilism, trade deficit, free trade, tariff, import certificate.

Address correspondence to Dr. Jesse T. Richman, Department of Political Science, Old Dominion University, BAL 7000, Norfolk VA, 23529 Tel: 757-683-3853 Fax: 757-683-4763, jrichman@odu.edu.

This article is in press: Estey Centre Journal of International Law and Trade Policy

The United States has run a trade deficit in goods and services for more than two decades. There have been important policy arguments about whether and to what extent balancing trade should be a policy priority. Classical economists believed that free market forces would correct trade imbalances “automatically.” But the evidence is clear that the U.S. trade deficit has been growing at a rapid pace during the last two decades and market forces have been largely ineffective in restoring a trade balance.[1]

Some economists attribute the enduring U.S. trade deficit to a new form of mercantilism by America’s trading partners, dubbed “monetary mercantilism” by Joshua Aizenman & Jaewoo Lee (2005), who defined it as “hoarding international reserves in order to improve competitiveness.” Under the classical form of mercantilism, countries encouraged their exports and discouraged their imports in order to build up their gold hoards. Under the new form, countries build up their foreign currency reserves as part of currency manipulations designed to encourage their exports and discourage their imports.

Japan had gradually invented monetary mercantilism in the years following World War II. Then Taiwan, the Asian Tigers and China copied the policy that had converted Japan from a weak and backward economy to a world powerhouse. In recent years, more and more countries have been joining the bandwagon, with the United States as their primary target. They have accumulated dollar assets in order to manipulate currency values and preserve the conditions that produce trade surpluses for them and trade deficits for the United States. China’s foreign exchange reserve buildups outstripped all of the others put together. Navarro and Autry (2011) summarized the disastrous effect of Chinese mercantilism upon the U.S. economy:

China's “weapons of job destruction” include massive illegal export subsidies, the rampant counterfeiting of U.S. intellectual property, pitifully lax environmental protections, and the pervasive use of slave labor. The centerpiece of Chinese mercantilism is, however, a shamelessly manipulated currency that heavily taxes U.S. manufacturers, extravagantly stimulates Chinese exports, and has led to a ticking time bomb U.S.–China trade deficit close to a billion dollars a day.

The belief in the U.S. is now widespread that free trade is not working. A solid majority of the American people favor steps that would shift U.S. trade toward a new policy. A December 2010 national poll (National Review/Allstate 2010) contained an extensive battery of questions on trade and U.S. manufacturing. The poll revealed strong public majorities against free trade. For example, 68 percent of respondents supported a policy requiring that “a certain percentage of every high-end manufactured product, such as automobiles, heavy machinery, and transportation equipment, sold in the U.S. be produced or assembled within the U.S., even if that means higher prices for their products.” Similarly, only 21 percent of respondents favored the pursuit of more free trade agreements, as opposed to 73 percent who favored either tariffs or subsidies to strengthen America’s competitive position.

Yet American policy makers and economists have been reluctant to take any action to balance trade. They have argued that the best response to mercantilism is a policy of unilateral free trade because mercantilism is a self-destructive strategy which eventually corrects itself. But if they are wrong, then the obvious response to mercantilist-produced trade deficits would be a counter-strategy which requires balanced trade. In this paper, we first discuss whether or not the modern form of mercantilism is a self-destructive and thus self-correcting strategy. Then we discuss mechanisms that a trade deficit country could utilize in order to produce balanced trade.

Is Mercantilism a Self-Destructive Strategy?

The Obama administration and the Federal Reserve have relied upon jawboning in order to persuade the Chinese government to change from its mercantilist strategy. For example, in his January 22 written testimony at his Senate confirmation hearing, Treasury Secretary designate Timothy Geithner (2009) indicated that he would seek to persuade China to change policy in its own self-interest:

More generally, the best approach to ensure that countries do not engage in manipulating their currencies is to demonstrate that the disadvantages of doing so outweigh the benefits. If confirmed, I look forward to a constructive dialogue with our trading partners around the world in which Treasury makes the fact-based case that market exchange rates are a central ingredient to healthy and sustained growth.

Federal Reserve Chairman Ben Bernanke (2010) gave similar advice to countries that were practicing monetary mercantilism:

Third, countries that maintain undervalued currencies may themselves face important costs at the national level, including a reduced ability to use independent monetary policies to stabilize their economies and the risks associated with excessive or volatile capital inflows.... Perhaps most important, the ultimate purpose of economic growth is to deliver higher living standards at home; thus, eventually, the benefits of shifting productive resources to satisfying domestic needs must outweigh the development benefits of continued reliance on export-led growth.

Geithner and Bernanke were echoing arguments given by the classical economists of the 18th and 19th century that mercantilism is a self-destructive strategy. But in his chapter about mercantilism in his 1936 magnum opus, The General Theory of Employment Interest and Money, Keynes questioned the conclusions of the classical economists. He reported that he had changed his own opinion after discovering that mercantilism works:

So lately as 1923, as a faithful pupil of the classical school who did not at that time doubt what he had been taught and entertained on this matter no reserves at all, I wrote: “If there is one thing that Protection can not do, it is to cure Unemployment. . . . There are some arguments for Protection, based upon its securing possible but improbable advantages, to which there is no simple answer. But the claim to cure Unemployment involves the Protectionist fallacy in its grossest and crudest form.” As for earlier mercantilist theory, no intelligible account was available; and we were brought up to believe that it was little better than nonsense. So absolutely overwhelming and complete has been the domination of the classical school. (p. 334)

Later in that chapter, Keynes summarized the argument for mercantilism from the standpoint of its practitioners and against mercantilism from the standpoint of its victims:

(A) favorable [trade] balance, provided it is not too large, will prove extremely stimulating; whilst an unfavorable balance may soon produce a state of persistent depression. (p. 338)

Other economists have experienced a similar change of position. For example, in their international economics textbook, Krugman and Obstfeld (2000) argued that classical economist David Hume had proven that mercantilism cannot work. But a decade later Krugman (2010) argued that the U.S. failure to respond to China’s “predatory trade policy” creates a “world in which mercantilism works.”

The classical argument against mercantilism had three components: (1) the comparative advantage argument of David Ricardo, (2) the reduced consumption argument of Adam Smith, and (3) the market forces balance trade argument of David Hume. We will discuss these three arguments in turn.

1. Ricardo’s Comparative Advantage Argument

The advantages of international trade based on comparative advantage are clear. Each country specializes in what it can produce with a comparative advantage and exchanges those for products that other countries produce with a comparative advantage. Each country trades a bundle of goods it can produce more efficiently for a bundle of goods the other country can produce more efficiently. In 1821, David Ricardo (1911) summarized the case for free trade as follows:

Under a system of perfectly free commerce, each country naturally devotes its capital and labour to such employments as are most beneficial to each. This pursuit of individual advantage is admirably connected with the universal good of the whole. By stimulating industry, by rewarding ingenuity, and by using most efficaciously the peculiar powers bestowed by nature, it distributes labour most effectively and most economically: while, by increasing the general mass of productions, it diffuses general benefit, and binds together, by one common tie of interest and intercourse, the universal society of nations throughout the civilized world. It is this principle which determines that wine shall be made in France and Portugal, that corn shall be grown in America and Poland, and that hardware and other goods shall be manufactured in England. (p. 81)

In this context, government interventions that distort market incentives are unambiguously bad. For instance, a tariff that limits trade would make both countries worse off than they otherwise would be. But what would be the result if trade is out of balance? What if Country A produces both those products with which it has a comparative advantage as well as those products that Country B produces with a comparative advantage and trades both to Country B in return for Country B’s IOUs?

And what if comparative advantage is not something fixed, such as the advantage that Portugal and France have with the production of wine in Ricardo’s example? What if comparative advantage in manufacturing is based upon economies of scale, as Gomory and Baumol (2000) demonstrated? Then can Country A obtain Country B’s comparative advantage?

Normally when trade is balanced, jobs that are lost competing with imports are replaced by even more productive and better paying jobs producing exports. But when trade is kept imbalanced by Country A, there are not as many jobs producing exports in Country B. Country A’s workers gain jobs and incomes, while Country B’s workers lose jobs and incomes. Country A gains industries and Country B gets debt.

2. Adam Smith’s Consumption Argument

Adam Smith deserves much credit for ending the era of mercantilism which dominated the economic policies of the European powers from the 16th through 18th centuries. According to that doctrine, the goal of economic policy was the accumulation of gold. To accomplish that end, mercantilist countries limited their imports and maximized their exports, which limited the growth in trade.

Smith’s chief argument, in his magnum opus Wealth of Nations, was that mercantilism hurts the economy of the country practicing it because it hurts consumers in order to benefit producers. He wrote:

Consumption is the sole end and purpose of all production; and the interest of the producer ought to be attended to only so far as it may be necessary for promoting that of the consumer. The maxim is so perfectly self-evident that it would be absurd to attempt to prove it. But in the mercantile system the interest of the consumer is almost constantly sacrificed to that of the producer; and it seems to consider production, and not consumption, as the ultimate end and object of all industry and commerce. (iv.8.49)

But Smith missed a short-run vs. long-run dimension. According to modern mercantilist theory, the mercantilist country sacrifices consumption in the short run in order to get even more consumption in the long run. The late University of Chicago Professor Jacob Viner (1948) laid out the twin goals of mercantilism as the following: (1) maximizing a country's power through accumulation of foreign assets and (2) maximizing long-term consumption by delaying present consumption in favor of future consumption.

In order to accomplish these ends it places tariffs (and other barriers) upon foreign products while at the same time buying foreign assets (mainly interest-bearing bonds today; gold in the past). In other words, mercantilist governments maximize their power and their people's future consumption through the combination of import barriers and foreign loans.

Heng-Fu Zou (1997), then a World Bank Senior Economist and now Dean of the China Economics and Management Academy at Central University in Beijing, demonstrated mathematically that Viner’s goals are compatible. First, he found that the more that the mercantilist country was willing to sacrifice present consumption by accumulating foreign assets, the more power the mercantilist government would gain and the more consumption the mercantilist people would have in the long-run. Second he found that the more successfully a mercantilist government applied tariff barriers to foreign consumer products, the more it would gain in wealth and power and the more its people would gain in long-run consumption.

Zou did not address the effect of mercantilism upon trading partners. In fact, he assumed for the purposes of mathematical tractability that the mercantilist country was a small economy with little effect upon its trading partners. But it is obvious that the effect upon the trading partner is exactly in reciprocal to the effect upon the country practicing mercantilism. The trading partner gets increased consumption in the short run in return for reduced consumption and power in the long-run.

3. David Hume’s Market Forces Balance Trade Argument

The third classic argument against mercantilism was the gold-flow theory presented by David Hume (1742) in Part II of his Essay on the Balance of Trade, an essay that influenced Adam Smith’s writing. Hume began:

Can one imagine, that it had ever been possible, by any laws, or even by any art or industry, to have kept all the money in SPAIN, which the galleons have brought from the INDIES? Or that all commodities could be sold in FRANCE for a tenth of the price which they would yield on the other side of the PYRENEES, without finding their way thither, and draining from that immense treasure? What other reason, indeed, is there, why all nations, at present, gain in their trade with SPAIN and PORTUGAL; but because it is impossible to heap up money, more than any fluid, beyond its proper level? The sovereigns of these countries have shown, that they wanted not inclination to keep their gold and silver to themselves, had it been in any degree practicable. (ii.v.12)

According to this argument, imbalanced trade cannot long last under a gold standard. If a trade surplus country collects gold from its trade deficit trading partners, the increased money supply in the trade surplus country would cause its wages and prices to go up. Meanwhile the reduction in the money supply in the trade deficit countries would cause their wages and prices to fall. The change in the relative costs of production would balance trade.

However, Hume never figured on the modern version of mercantilism in which the government of the mercantilist country stocks up on the currency of the deficit country and uses it to buy financial assets in the deficit country. These are acts which are appropriately called mercantilism because they are intended to perpetuate the surplus of exports over imports and they short-circuit the normal market correction no matter whether the world is on a gold standard or on a standard of freely traded currencies.

A modern version of Hume’s argument holds that the capital inflows that accompany trade deficits benefit the country that receives the capital. When one country has higher returns on capital (i.e., higher interest rates), capital tends to flow into it. This capital will produce fixed investment, as did the inflow of capital to the United States during the 19th century or the inflow of capital that helped rebuild Europe after World War II. The resulting economic growth will make up for the temporary trade deficits and balance trade in the long-run.

But while private capital indeed flows to where it can obtain the highest return, public capital does not. Mercantilist governments buy foreign financial assets even when the rates of return on capital are higher in their own country than abroad. They even suppress their own people’s access to credit in order to collect this capital and make loans abroad.

Moreover, the effect on the recipient country of financial inflows may be detrimental. Prasad, Rajan and Subramanian (2007) found that the more a nonindustrial country was importing financial capital, the slower its growth. They concluded that the deleterious effect of the foreign capital is due to the resulting higher exchange rate that makes the recipient country’s exports less competitive in world markets. They wrote:

To summarize, we have presented evidence that capital inflows can result in overvaluation in nonindustrial countries and that overvaluation can hamper overall growth. To bolster this claim, we have shown that overvaluation particularly impinges on the growth of exportable industries.

Despite the empirical evidence that foreign financial capital hurts nonindustrial countries, Prasad et al. contended, without providing any evidence, that the inflow of financial capital may benefit industrialized countries. Indeed this is possible, but foreign capital only makes an economic contribution to growth and employment when it is invested in new productive assets. The purchase of financial and existing assets instead leads to house or stock price bubbles or increased consumption of consumer goods, providing only short-term benefit. Eventually, the loans must be paid back with interest even though they have already adversely affected the industries that compete in world markets.

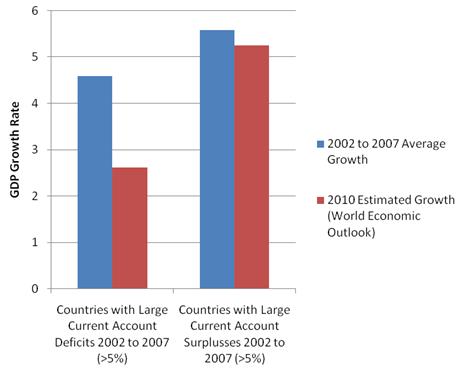

Figure 1 illustrates a similar pattern in an analysis of all world economies running trade deficits or surpluses in excess of five percent of GDP. When countries run large current account deficits they accumulate debt in one form or another. And this debt can later cause serious economic harm. It compares the growth rates of countries that ran large average current account deficits (more than five percent of GDP) in the 2002 to 2007 period with growth rates for countries that ran large current account surpluses during this period (more than five percent of GDP).

For the 2002 through 2007 period there are differences -- the average growth rate was higher for countries with surpluses. The differences are even more pronounced in the 2010 growth estimates. Countries with a history of running trade surpluses have recovered rapidly from the 2008 financial crisis and recession and are growing quickly. Countries with a history of running current account deficits have not. This is the pattern Keynes (1936) predicted, and it directly contradicts classical theory.

Figure 1. Consequences of Current Account Deficits and Surplusses for Economic Growth (IMF data: analysis by the authors)

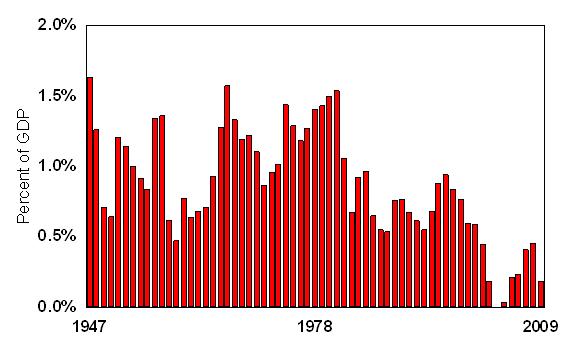

In the case of the United States, it is not clear that the net loans associated with trade deficits provided investment benefits. Indeed, it is possible that such loans simultaneously lowered interest rates and took away investment opportunities during the 1998-2009 period. Figure 2 shows that net investment in American manufacturing, which averaged 1.00% of U.S. GDP per year from 1947 through 1996, fell to just 0.35% of GDP from 1998-2007..

Figure 2. Net Manufacturing Investment in the United States (source BEA tables 3.7ES, 3.6ES and 1.1.5).

In summary, although monetary mercantilism reduces short-term consumption, it increases long-term consumption and power in the mercantilist country. Meanwhile, it has the exact opposite effect upon its trading partners giving them short-term gains in consumption combined with long-term losses in consumption and power. Furthermore, market mechanisms do not correct the resulting trade imbalances, nor do they compensate for the long term shift in production and consumption towards the mercantilist.

Mechanisms for Balancing Trade

What if a country is trading with mercantilist trading partners and doesn’t wish short term gains in consumption in return for long-term losses in consumption and power? What can the trade deficit country do? There are a variety of approaches that it might take. In this section we present four interventions in free markets that have been proposed in order to balance trade. All aim to counter mercantilism without becoming mercantilist. The first two proposals utilize import licenses, called Import Certificates (ICs), to balance trade. The second two proposals utilize tariffs. The proposal which we believe most likely to succeed is the scaled tariff.

1. Buffett Import Certificate Plan

Financier and businessman Warren Buffett first proposed ICs to balance trade in a Fortune Magazine article (Buffett & Loomis, 2003). His proposal may have been modeled upon the “cap-and-trade” plans that had successfully reduced pollution, but instead his plan would cap imports to the level of exports, thereby balancing trade. Buffett wrote:

We would achieve this balance by issuing what I will call Import Certificates (ICs) to all U.S. exporters in an amount equal to the dollar value of their exports. Each exporter would, in turn, sell the ICs to parties – either exporters abroad or importers here – wanting to get goods into the U.S. To import $1 million of goods, for example, an importer would need ICs that were the byproduct of $1 million of exports. The inevitable result: trade balance

Under the Buffett Plan, whenever American producers exported American products abroad, they would earn ICs that they could profitably sell to prospective importers. Meanwhile, imports would face the additional cost of the required ICs.

In September 2006, Senators Byron Dorgan and Russ Feingold fleshed out the Buffett Plan into bill form, which they named the Balanced Trade Restoration Act of 2006. Their bill would have the Department of Commerce issue ICs (which they called “Balanced Trade Certificates”) directly to exporters.

Each $1 of exports (based upon the appraised value declared on the shipper’s export declaration) would earn the exporter a $1 IC which the exporter could then freely market to importers of goods to the United States. The value of imports allowed by an IC would change over time. During the first year of the program, a $1 certificate would allow up to $1.40 of imports, during the second year, $1.30 of imports, the third year $1.20, and so on until by the fifth year $1 of exports would allow $1 of imports. The exporters would freely market the ICs to those who wished to import goods and the Commerce Department would require that the certificates be submitted with imports.

Dorgan and Feingold’s bill exempted oil and gas imports from the IC requirement during the first five years of the program and then phased them in thereafter, perhaps so that, as Papadimitriou, Hannsgen, and Zezza (2008) pointed out, the ICs would be less expensive, since demand for fuel products is relatively inelastic. On the other hand, requiring ICs for fuel imports would have given American consumers an incentive to conserve fuel products and American producers an incentive to produce more fuel products.

2. Targeted Import Certificate Plan

Richman et al. (2008) developed a Targeted IC Plan in which the ICs would be auctioned by the government and would be country specific. The targeted ICs were designed to gradually balance trade over a five year period with countries that practice mercantilism, as evidenced by excessive foreign exchange reserve accumulations by their governments. It had five provisions:

- Auctioned in the open market. The targeted ICs would be auctioned monthly by the Treasury Department in the open market.

- Expire in six months. Each targeted IC would expire if not used within six months of the date that it was issued and would not be tradable in the open-market.

- Each targeted IC permits a certain value of imports. Possession of the targeted IC by physical or electronic means would enable the bearer to import a specific value of goods or services from the targeted country. Each targeted IC could only be used once.

- Reduce trade imbalance over five years. The targeted ICs would be issued in the proper quantities in order to gradually reduce the maximum trade-ratio between American exports to a country and American imports to that country over a five year period. The trade-ratio every year during the first five year period would be lower than the trade ratio of the preceding year, but the rate of decline from month to month would be set by the Treasury Secretary.

- Not needed when trade approaches balance. Whenever the actual trade-ratio would fall below 1.05:1 over a calendar year, the Treasury Secretary would cease auctioning the targeted ICs and would cease requiring that they accompany imports of goods and services from the targeted country. If, after that, the trade-ratio increases to over 1.15:1 over a calendar year, the targeted IC program could be re-instated with that country at the discretion of the Secretary of the Treasury.

Targeted ICs preclude trade retaliation. If a mercantilist government were to respond with counter-restrictions of its own, it would actually be reducing the amount of its own exports to the country issuing the certificates.

3. Currency Rate Reform Bills

During the 2009-2010 Congress, two currency rate reform bills were proposed to target currency manipulations. The Currency Exchange Rate Oversight Reform Bill was introduced by Senator Charles Schumer and the Currency Reform for Fair Trade Act was introduced by Representative Timothy Ryan.

Each bill had a different method for determining whether a country was manipulating its currency and the extent of those manipulations. The Senate bill relied upon the Treasury Secretary to make that determination, while the House bill relied upon statistics that are voluntarily reported by governments to international organizations.

Both bills provided for the U.S. Commerce Department to assess the amount that a currency is overvalued when deciding individual industry by industry anti-dumping and countervailing duty suits. The result would be many suits on the Commerce Department’s docket that would be expensive and time consuming for each individual industry to put together. Any tariffs that would be applied would be piece-meal, not across the board.

4. Scaled Tariff

University of Maryland business professor Peter Morici (2008), a former director of the Office of Economics at the U.S. International Trade Commission, was the first to propose a tariff whose rate would go up or down depending upon actions that cause a trade deficit. He proposed a dollar-yuan conversion tax that would be applied to Chinese imports into the United States at a rate that would be adjusted to the rate of Chinese currency market interventions. He wrote:

China subsidizes exports by selling its currency, the yuan, for dollars at artificially low values in foreign-exchange markets, making Chinese goods artificially cheap at Wal-Mart. The U.S. government should tax dollar-yuan conversions at a rate equal to China's subsidy until China stops manipulating currency markets. That would reduce imports from, and increase exports to, China.

However, the central bank involved in these currency market interventions may or may not choose to report them. China, for example, only reports the dollar value of its foreign exchange reserves to international organizations, not their currency composition.

Moreover, China is not the only country that intervenes in currency markets in order to manipulate currency exchange rates. Bernanke’s (2010) Figure 8 shows that 13 of the 16 emerging market governments that Bernanke considered had devoted more than 3% of their countries’ GDP to currency market interventions (i.e., accumulating currency reserves) from September 2009 to September 2010.

We have proposed a Scaled Tariff that is similar to Morici’s proposal. But instead of being designed to take in 100% of voluntarily reported currency conversions as tariff revenue, it is designed to take in 50% of the bilateral trade deficit (goods plus services) as revenue. It would be applied to all countries that have had a sizable trade surplus with the United States over the most recent four economic quarters.

The country with both a current account deficit and a foreign debt would simply charge the Scaled Tariff at the appropriate duty rates upon imported goods from the trade surplus countries while rebating Scaled Tariff payments to United States exporters to the extent that they were paid on inputs to those particular exports.

Here's how the numbers of the Scaled Tariff would work with China in a particular year. In 2009 the United States imported $305 billion of goods and services from China, while China imported $86 billion of goods and services from the United States, creating a trade deficit of $219 billion. An initial tariff rate of 37% on $297 billion of imported goods from China would be designed to collect $109.5 billion (50% of $219 billion) in tariff revenue, if the trade deficit were to continue at the 2009 level.

The specifics of the Scaled Tariff, if enacted by the United States, would be the following:

1. Applied only to goods. The Commerce Department would charge the Scaled Tariff on all Goods originating from each country that with which the United States had a sizable trade deficit in goods and services of at least $500 million over the most recent four quarters. The rate would be applied upon the declared dollar value of such goods on the entry summary form.

2. Rate of duty designed to take in 50% of trade deficit. The rate of the duty would be adjusted quarterly and calculated as the rate that would cause the revenue taken in by the duty upon imported goods from the particular country to equal 50% of the trade deficit (both goods and services) with that country over the most recent four economic quarters.

3. Rebated to exporters. The Commerce Department would rebate Scaled Tariff payments to U.S. exporters to the extent that they were paid on inputs to those particular exports.

4. Suspended when trade reaches balance. The Scaled Tariff would be suspended whenever the Commerce Department determined that during the most recent calendar year the current account of the United States was in surplus. Collection would resume when the Commerce Department determined that during the most recent calendar year the current account deficit of the United States was at least 1% of United States GDP.

The Scaled Tariff differs from the currency reform bills in that: (1) the duty rate is determined from readily available statistics that each country collects about its own trade, (2) the rate of the duty gets reduced as trade moves toward balance, and (3) the duty rate is applied across-the-board to all goods arriving from that country.

Comparison of the Balanced Trade Plans

In this section, we will discuss the four proposals in terms of their benefits, their administrative costs, and their legality under international law.

Benefits of the Plans

The Buffett Plan, the Targeted IC Plan and the Scaled Tariff are all designed to balance trade. The currency reform bills only balances trade if mercantilist countries decide to give up their trade manipulations in response. If they instead decide to respond with counter tariffs, the currency reform bill reduces exports as well as imports.

Not all of the plans produce perfectly balanced trade. The Buffett Plan provides a guaranteed path to balanced trade since, after a certain period of time, it only permits imports that total the same value as exports into a country. The Targeted IC Plan only applies to currency manipulating countries, so it only balances trade with those countries and allows trade from the currency manipulating countries to be routed through a non-trade manipulating country.

The Scaled Tariff would largely balance trade since it applies to all countries with which a trade deficit country has significant trade deficits. If trade to a trade deficit country is rerouted by a trade surplus country through a non-trade-surplus country, it can produce a trade surplus in that country which causes the Scaled Tariff to be applied to that country’s products.

The Buffett Plan has the additional benefit of providing export subsidies from the sale of the ICs to the trade deficit country’s exporting industries. In a commentary endorsing Buffett’s plan, Ralph Gomory (2010) pointed out that balancing trade and rewarding productivity are the two components that are needed in order for a country to recover industries that it has been losing due to manipulations of manufacturing comparative advantages.

In a Levy Economics Institute working paper, Papadimitriou et al. (2008) analyzed the costs and benefits of the Buffett Plan, making quantitative estimates of the effects. They pointed out that the Buffett Plan would cause an immediate macroeconomic boost to the economy, increase profits of businesses that produce for export, increase government tax collections (because of increased American income), and reduce the trade deficits to a sustainable level.

The Targeted IC Plan and the Scaled Tariff would also revive exporting industries by increasing exports, although neither plan would provide the direct subsidies associated with the Buffett Plan. If the mercantilist governments refused to increase their imports, then the trade deficit country would increase its imports from countries that themselves import more when their economy grows.

All but the currency manipulation bills would provide significant amounts of government revenue from tariffs or the selling of the ICs in the first years of the plan. That government revenue would be gradually replaced by increased income by producers of tradable goods as investments in new production would move trade toward balance.

The currency reform bills, however, would only provide a modest boost to government revenue and to the income of import-competing industries. If the currency-manipulating countries retaliated by further restricting their imports, these bill could end up protecting import-competing industries at the expense of exporting industries.

Administrative Costs

The currency reform bills require that each industry seeking tariffs put together a legal anti-dumping case that would be adjudicated by the Commerce Department. Such procedures are expensive, both to the Department and to the affected industries.

The two IC plans require that a new government bureaucracy be set up to administer the ICs. In addition, they add a new cost to businesses, the cost of obtaining the ICs in order to obtain imports. Papadimitriou et al. argue that these costs would produce significant uncertainty on the part of businesses needing imported products. But importers and exporters already deal with future uncertainty in foreign trade due to changing exchange rates. But both IC plans would place expiration dates upon the ICs so that the futures market for ICs would be liquid.

Papadimitriou et al. also pointed out that if, as under the Buffett Plan, ICs could be earned by service exports, not just goods exports, this would create a large incentive to fraudulently obtain ICs from intra-corporate transactions. The Targeted IC Plan and the Scaled Tariff avoid this problem because they do not provide export subsidies.

The Scaled Tariff has the lowest administrative costs of all of the plans. Countries already calculate the trade statistics that are used to determine the duty rate. Countries already have customs at their borders that determine the value of imported goods. There is no danger of ICs losing liquidity, since there would be no ICs. The administrative cost would be negligible.

Legality under International Law

In an Economics Policy Institute working paper, Stewart and Drake (2009) discussed the legality of the various IC plans in terms of international law. They held that auctioning ICs, as in the Targeted IC Plan, would be more consistent with WTO rules than distributing them to exporters because providing the certificates to exporters would lead to “potential inconsistencies with WTO prohibitions on export subsidies.”

They also discussed the legality of the IC plans with regard to Article XII of GATT 1994, annexed to the Agreement Establishing the World Trade Organization. This framework permits any country that has (1) a perilous external financial position and (2) a balance of payments deficit in the current account to restrict the quantity or value of merchandise permitted to be imported in order to bring payments toward balance. Even though the United States was a net foreign creditor in 1971, IMF and GATT agreed that the United States had a perilous financial position simply because its reserves only equaled the value of about three months worth of imports. As Stewart and Drake noted, the IC plans met the basic criteria of the Article XII framework for two primary reasons:

First, the program is specifically designed to limit imports only to the extent needed to restore equilibrium to the trade balance. It is thus consistent with provisions in Article XII that require countries to limit import restrictions to those necessary to address balance-of-payments problems and that urge countries to take steps to restore equilibrium in their balance of payments on a sound and lasting basis. (p. 11)

Second, the program does not distinguish between products, and thus it is not designed to provide special protective benefits for certain domestic industries. The program is therefore consistent with Article XII provisions regarding the avoidance of “uneconomic employment of productive resources,” as well as with provisions in the 1994 Understanding that require import restrictions to control the general level of imports, to minimize incidental protective effects, and to be transparent. (p. 11)

However, they noted that the Buffett Plan, but not a Targeted IC Plan, would comply with another Article XII provision, one that prohibits targeting of specific countries, especially poor countries. Stewart and Drake wrote:

Third, the [Buffett] program does not distinguish between countries, and thus it does not unduly disadvantage some countries to the benefit of others. This approach is consistent with Article XII provisions regarding the avoidance of unnecessary damage to trading partners. While the proposal does not exempt imports from less-developed countries as suggested in the 1979 Declaration, this is not a mandatory requirement, and the advantages of universal application may outweigh the benefits of special and differential treatment in this regard. (p.11)

On the other hand, targeting currency manipulators would be consistent with the International Monetary Fund Articles of Agreement which require (Article IV) that countries “avoid manipulating exchange rates or the international monetary system in order to prevent effective balance of payments adjustment or to gain an unfair competitive advantage over other members.” And the International Monetary Fund would be involved whenever a country invokes Article XII. as Stewart and Drake note:

In any case, imposition of a trade balancing program under Article XII will precipitate consultations at the WTO and may lead to a challenge under WTO dispute settlement procedures. Given the deference the WTO accords to IMF determinations regarding balance-of-payments issues in such proceedings, implementation should also be accompanied by U.S. efforts to explain the policy to Fund officials. (p. 12-13)

In contrast, it is not clear whether the currency reform bills would be consistent with WTO rules. They would be imposed under anti-dumping provisions even though the WTO has not yet recognized that currency manipulation qualifies as dumping.

Of all the plans, the Scaled Tariff may be the most consistent of all with the Article XII framework for three reasons:

- Article XII expressly permits import duties that are in excess of the duties inscribed in the WTO schedule for a member.

- Article XII requires that countries relax their import duties as the trade deficit grows smaller. The Scaled Tariff’s rate goes down as trade with a country approaches balance and disappears entirely when bilateral trade approaches balance or the balance of payments in the current account reaches balance.

- Article XII does not allow unfair targeting of specific countries. The duty set by the Scaled Tariff is fairly set as the rate required to earn 50% of the value of the bilateral trade deficit with each country.

Conclusion

Monetary mercantilism reduces the short-term consumption in the mercantilist country while increasing its long-term consumption and power. It has the exact opposite effect upon its trading partners giving them short-term gains in consumption combined with long-term losses in consumption and power. Market mechanisms do not correct the resulting trade imbalances.

The classical argument that mercantilism is a self-defeating strategy only applied to the classical form of mercantilism. Monetary mercantilism is a self-sustaining successful strategy. When the country practicing mercantilism intervenes in currency markets to buy foreign currencies and then lends those currencies back to its trading partners, market mechanisms do not correct the resulting trade imbalances.

In this paper, we have discussed four mechanisms to balance trade, two of which rely upon Import Certificates, while the other two rely upon tariffs. The mechanisms differ in six respects, with the Scaled Tariff excelling in each:

- Balanced Trade. The Buffett Plan and the Scaled Tariff balance trade. The Targeted IC Plan could let trade surplus countries reroute trade through non-targeted countries. The currency reform bills could simply result in a reduction in trade.

- Exporting Industries. The Scaled Tariff and the Targeted IC Plan encourage exports by changing the incentives to mercantilist countries. The Buffett Plan encourages exports by providing export subsidies.

- Government Revenue. The Scaled Tariff and the Targeted IC Plan provide a significant amount of government revenue.

- Counter-Tariffs. The Scaled Tariff and the Targeted IC Plan discourage counter-tariffs. A trade surplus country that responds with counter-tariffs would be further restricting its own exports.

- Administrative Costs. Only the Scaled Tariff is free of administrative costs. The Buffett Plan and the Targeted IC Plan require that a new government bureaucracy be set up and that firms wishing to import obtain ICs. The currency reform bills have the costs associated with prosecuting and adjudicating a separate anti-dumping case for each industry.

- WTO Rules. Only the Scaled Tariff would clearly comply with WTO rules. It closely follows the provisions of Article XII of GATT 1994, annexed to the Agreement Establishing the World Trade Organization. The tariffs under the currency reform bills could violate WTO rules. The export subsidies of the Buffett Plan could violate WTO rules. The Targeted IC Plan could violate the provision in the WTO rules against targeting specific countries, but they could be justified as being enforcement procedures under the IMF rule against currency manipulations.

The effects of the Scaled Tariff upon international trade would be quite beneficial. During the 1940s, John Maynard Keynes tried to establish a world trade system based upon balanced trade. Volume 25 of his collected writings (Keynes, 1980) is full of his plans for the institution that would regulate the world economy after World War II. Both the IMF and the WTO were founded, partly based upon Keynes' advice. But the institution that Keynes would have created would have required that trade surplus countries take down their trade barriers while letting trade deficit countries use export subsidies, import restrictions, and tariff barriers to bring trade into balance.

Keynes had anticipated that there would be a huge growth in world trade after World War II and wanted to insure that it would be balanced, so that it could continue to grow. He realized that imbalanced trade eventually leads to financial crises in the trade deficit countries, such as the financial crises that engulfed the United States, Greece, Portugal and Spain beginning in 2008.

If the United States were to implement a Scaled Tariff, other trade deficit countries would likely follow suit. The world trade system would once again be placed on a sound financial basis since balanced trade can grow forever, but trade imbalances eventually produce financial crises in the trade deficit countries which ruin the markets for the trade surplus countries. The scourge of beggar-thy-neighbor mercantilism would finally be ended.

References

Aizenman, Joshua and Jaewoo Lee (2006), “Financial versus monetary mercantilism – long-run view of large international reserves holding,” NBER Working Paper No. 12718.

Allstate/National Journal (2010), Heartland Monitor Poll VII, www.allstate.com/Allstate/content/refresh-attachments/Heartland_VII_Topline.pdf

Bernanke, Ben S. (2010). Rebalancing the Global Economy. Speech given at the Sixth European Central Bank Central Banking Conference, Frankfurt, Germany

Buffett, Warren E. & Carol J. Loomis (2003) “America’s Growing Trade Deficit is Selling the Nation Out from Under Us. Here’s a way to Fix the Problem -- And We Need to Do It Now,” Fortune, November 10.

Geithner,Timothy (2009). Written response to questions from Senate Finance Committee, January 22.

Gomory, Ralph E. and William J. Baumol (2000), Global Trade and Conflicting National Interests. Cambridge: The MIT Press.

Gomory, Ralph E. (2010), “A time for action: Jobs prosperity and national goals”, Huffington Post, www.huffingtonpost.com/ralph-gomory/a-time-for-action-jobs-pr_b_434698.html

Hume, David (1742).Part II, Essay V, Of the Balance of Trade.

Keynes, John Maynard (1937) General Theory of Employment Interest and Money. NY: Harcourt, Brace and Company.

Keynes, John Maynard (1980) The Collected Writings of John Maynard Keynes Economics Articles and Correspondence: Activities 1940-1944: Shaping the post-war world, Volume 25, London: McMillan.

Krugman, Paul and Maurice Obstfeld (2000), International Economics: Theory and Policy 5th Edition, Glenview, IL: Little, Brown.

Krugman, Paul (2010), Killer Trade Deficits, August 16, 2010. http://krugman.blogs.nytimes.com/2010/08/16/killer-trade-deficits/

Morici, Peter (2008), “Americans must live within their means,” Philadelphia Inquirer, April 6.

Navarro, Peter W., and Greg Autry (2011), Death by China: Confronting the Dragon - A Global Call to Action, NY: Pearson Prentice Hall.

Papadimitriou, Dimitri B., Greg Hannsgen and Gennaro Zezza (2008), The Buffett Plan for Reducing the Trade Deficit, The Levy Economics Institute at Bard College, Working Paper No. 538.

Prasad, Eswar S., Raghuram G. Rajan, and Arvind Subramanian, “Foreign Capital and Economic Growth” (NBER Working Paper No. 13619, November 2007): 31

Ricardo, David (1911) The Principles of Political Economy and Taxation, London: J.M. Dent & Sons.

Smith, Adam (1776) An Inquiry into the Nature and Causes of the Wealth of Nations.

Stewart, Terence P. & Elizabeth J. Drake (2009), Addressing Balance of Payments Difficulties Under World Trade Organization Rules. Economic Policy Institute Working Paper #288.

Triffin, Robert (1960) Gold and the Dollar Crisis: The Future of Convertibility, New Haven: Yale University Press.

Viner, J. (1948) Power versus plenty as objectives of foreign policy in the seventeenth and eighteenth centuries. World Politics 1.

Zou, Heng-Fu (1997) “Dynamic Analysis of the Viner Model of Mercantilism,” Journal of International Money and Finance 16.

Footnotes:

[1] Some economists, following Robert Triffin (1960), assume that trade deficits are inevitable in the country whose currency serves as the world’s reserve currency. But there is nothing inevitable about it. When trade is balanced, a country earns enough foreign exchange to pay for its imports. In any case, it is not necessary to have a favorable balance of trade to create reserves, although countries may prefer to build reserves by a surplus of exports over imports employing mercantilist barriers to imports. After all, reserves can also be created by currency swaps with the U.S. building comparable reserves of foreign currencies. Bernanke’s currency swaps in October 2008 demonstrate this. After the Federal Reserve closed Lehman Brothers without protecting its creditors, the dollar spiked upwards in currency markets due to a sudden international dollar deflation. As a result, many foreign businesses that had borrowed money in dollar-denominated loans couldn’t make their payments. The Federal Reserve offered currency swaps to many of the world’s central banks, who in turn made those dollars available to their businesses so that they could avoid bankruptcy. Two-sided currency flows can provide international liquidity without requiring trade imbalances.